Initiatives for the environment Addressing climate change

We regard environmental issues, including climate change, as important management challenges, and in June 2019, we declared our support for the TCFD recommendations. We strive for transparent disclosure of each of “Governance,” “Strategy,” “Risk Management,” and “Numerical Targets and Goals,” items included in the TCFD recommendations for disclosure.

Governance

The Group has been strengthening the structure to manage and promote SDG-related initiatives towards realization of sustainable local communities and its own value creation. On the management side, it established the Sustainability Promotion Committee, and the committee reports the progress in SDGrelated initiatives every three months. The Sustainability Promotion Committee is led by the chair, who is the president and representative director, and vice chair, who is the officer in charge of the Corporate Planning Division, and its members consist of representative directors, managing executive officers and above, and all general managers. The members present reports and engage in discussions with the general manager of the Internal Audit Division and Audit and Supervisory Committee members as observers. The Group Management and Execution Council decides new SDG-related measures, etc. through thorough discussions and deliberations. Matters for reporting by the Sustainability Promotion Committee and matters for deliberation by the Group Management and Execution Council are reported and resolved at the Board of Directors Meeting on a regular basis and they are being supervised by the Board of Directors. On the promotion side, the Company has established the Sustainability Management Office and Higo Bank and Kagoshima Bank the Sustainability Promotion Office, through which the Group companies are closely collaborating to spread and promote SDGs throughout the Group.

[Climate Change Initiatives]

| Participation in initiatives | Establishment of internal policies | ||

| June 2019 | Support for TCFD recommendations | July 2019 | Establishment of Guideline for Investments and Loans |

| December 2020 | Establishment of Environmental Policy | ||

| April 2021 | Establishment of CO2 reduction targets | ||

| February 2022 | Establishment of Sustainable Investment and Loan Policy | ||

| March 2022 | Endorsement of the GX League Basic Concept | ||

| May 2022 | Membership in PCAF | ||

| April 2023 | Participation in the GX League | March 2023 | Carbon Neutrality Declaration |

| April 2024 | Establishment of the Biodiversity Conservation Policy | ||

Strategies

The Group regards environmental issues, including climate change, as important management challenges. In June 2019, it declared its support for the TCFD recommendations and has been pursuing transparent disclosure on its website and through its integrated report. In September 2020, the Group signed the Principles for Responsible Banking (PRB) advocated by the United Nations Environment Programme Finance Initiative (UNEP FI) to align its business with SDGs and has been striving to promote sustainable finance.

(1) Risks and opportunities

The Group is aware that risks arising from climate change affect its business operation, strategies, and financial plan. While working on climate-related risk management by utilizing scenario analysis, etc., the Group considers the reduction of GHG emissions at customers and investment and loans for improvement of energy efficiency (sustainable finance) for the realization of a carbon-free society as business opportunities and will proactively implement financial initiatives aimed at reducing the environmental burden.

(2) Formulation of transition plan

As a regional value co-creation group that plays a significant role in realizing a carbon-free society in the region, the Group aims to achieve carbon neutrality (scope of calculation: the Company and its wholly owned subsidiaries) for Scope 1 and 2 emissions by FY2030. In addition to the initiatives and measures within the Group, it formulated a transition strategy for supporting decarbonization efforts in the region and customers. In FY2023, the Ministry of the Environment selected the Group for the portfolio carbon analysis support project, in which it analyzed and grasped total CO2 emissions at its borrowers and investees and discussed the transition strategy for the livestock industry, a sector with high emissions. The Group follows the standards set by the Partnership for Carbon Accounting Financials (PCAF), an international initiative that it joined in May 2022, for the calculation of CO2 emissions by borrowers and investees, and will continue to work on the enhancement of disclosure. Higo Bank established KS Energy Co., Ltd. in January 2024, a wholly-owned subsidiary engaged in the renewable energy business. In addition, the bank developed a CO2 emission measuring system, the Zero-Carbon-System (Tansaku-kun), and started offering the service. In April 2024, Kagoshima Bank concluded a partnership agreement for the promotion of GX in the livestock industry and industrial development of Kagoshima Prefecture in collaboration with industry, academia, government, and financial sector, and it is implementing the initiative to reduce GHG emissions from cattle as well as reduction of production costs and improvement of productivity. The Group will deepen its knowledge of decarbonization and other environmental issues and continue to promote initiatives for visualizing and reducing CO2 emissions in the region and by its customers.

(3) Scenario analysis

To grasp the concrete impact of climate change on the business, Higo Bank and Kagoshima Bank carried out a scenario analysis through 2050 and upgraded and refined the scenario analysis for the Group as a whole. The Group recognizes physical risks and transition risks as climate-related risks and assumes an increase in credit costs from damage to assets caused by extreme weather risks as physical risks and an increase in credit costs with respect to customers who are likely to be affected by strengthening of restrictions caused by climate changes and changes in consumption preferences as transition risks.

[Physical risk]

Based on the 8.5 scenario (4°C scenario) by the Intergovernmental Panel on Climate Change (IPCC), the Group calculated the impact on credit costs of floods, which account for the majority of natural disasters resulting from climate change and are especially highly likely to occur in Kyushu. The increase in credit costs through 2050 was calculated at as much as 6.6 billion yen based on the estimate of damage to value resulting from damage to collateral real estate set by Higo Bank and Kagoshima Bank caused by floods, etc. (direct impact) and the estimated number of days of business suspension at customers caused by damage to buildings.

| Direct impact (devaluation held collaterall) |

Indirect impact (worsening of customer earnings due to business stagnation) |

|

| Risk event | Flood | |

| Scenario | 4°C Scenario* 1 | |

| Local community | Kumamoto Prefecture, Kagoshima Prefecture, Miyazaki Prefecture | |

| Risk indicator | Credit cost | |

| Analysis results* 2 | Increase in credit cost: 1,700 million yen | Increase in credit cost: 4,900 million yen |

* 1 Inundation height of each asset and damage depending on inundation height were calculated using the hazard map and Manual for Economic Evaluation of Flood Control published by the Ministry of Land, Infrastructure, Transport and Tourism.

* 2 Based on RCP 8.5 scenario by IPCC.

[Transition risk]

The Group quantified transition risks of the energy sectors defined by the TCFD recommendation. It calculated an increase in credit cost of its borrowers in the selected sector from the impact of carbon tax, energy price, and change in product mix on operating expenses at borrowers and the impact on their sales from changes in demand. As a result, the increase in credit costs through 2050 came to be as much as 14.6 billion yen per single fiscal year. Going forward, the Group will refine the transition risks through expansion of analysis target.

| Direct impact | |

| Scenario | 1.5℃ Senario* |

| Scope of analysis | Part of the energy sector defined by TCFD |

| Local community | Japan |

| Analysis period | Through 2050 |

| Risk indicator | Credit cost |

| Analysis results | As much as 14.6 billion yen per single fiscal year |

- It is based on the Net Zero Emissions by 2050 Scenario (NZE) by the International Energy Agency (IEA). However, the Group supplemented Japan’s scenario data that is not included in the NZE scenario using the Announced Pledges Scenario (APS), etc. as necessary.

(4) Carbon-related assets

The ratio of carbon-related sectors* to loans of the Group is as shown in the table on the below.

| Energy | Transport | Materials and buildings | Agricultural, food and forestry products |

| 1.96% | 2.14% | 10.49% | 3.04% |

-

Classified using the TCFD recommendation, Japanese Standard Industrial Classification, industry codes of Higo Bank and Kagoshima Bank, etc. [Energy] Oil and gas, coal, electric utilities (excluding renewable energy power generator, independent power producers, and water utilities) [Transportation] Air freight, passenger air transportation, maritime transportation, rail transportation, trucking services, automobiles and components

[Materials and buildings] Metals and mining, chemicals, construction materials, capital goods, real estate management and development

[Agriculture, food, and forest products] Beverages, agriculture, packaged foods and meats, paper and forest products

The Group's main risks and opportunities considering physical risks and transition risks

The Group analyzed risks and opportunities associated with climate change in the time frames of short term (within three years), medium term (three to 10 years), and long term (10 years and longer).

(Risks)

- Suspension of business activities and property damage at customers due to exacerbation of extreme weather affect the customers' business and financial standings, which may damage the value of the Group's loan assets. (Short to long term)

- The corporate evaluation of the Group may decline as a result of its responses to environmental issues being inferior to those of competitors. (Short to long term)

- The value of the Group's loan assets may be damaged as climate change-related policies such as carbon tax and oil and coal tax increase and tightening of restrictions on greenhouse gas (GHG) emissions and energy efficiency rate of newly constructed buildings affect its customers' businesses and financial standings. (Medium to long term)

(Opportunities)

- Fund demand is expected to increase for customers' capital investment towards decarbonization including spread of renewable energy in the energy sector, introduction of highly efficient construction methods and low-carbon construction materials in the real estate sector, spread of electronic vehicles and expansion of low carbon technologies in the automobile and transportation sectors. (Short to long term)

- The opportunities to offer insurance products in preparation for natural disasters and financial products and services related to environmental conservation are expected to increase due to exacerbation of natural disasters and changes in customers' behavior due to improved environmental awareness. (Short to long term)

- Funds demand is expected to increase throughout all sectors for additional infrastructure investment in disaster prevention facilities at customers due to exacerbation of extreme weathers. (Medium to long term)

Risk management

Taking into consideration the results of scenario analysis, the Group recognizes the possibility that climate change risks can impact its financial affairs and is implementing the following initiatives.

(1) Risk capital allocation

The Group considers climate change risks as risks associated with external factors, and added physical risks to the stress scenario when calculating credit risks starting FY2023. It has confirmed the sufficiency of the capital for physical risks in the event an assumed scenario becomes reality.

(2) Investments and loans

Upon making investment and providing loans, the Group, in the Sustainable Investment and Loan Policy, stipulates that as a rule it refrains from making investment in businesses that are highly likely to have negative impact on climate changes such as coal fired thermal power generation and logging. In the review for providing loans, etc., the branch involved and the loan-related division that performs the loan review carry out the checking and make loan judgment by factoring in the impact on climate change. The Group will further deepen scenario analysis throughout the organization and work to quantify climate change risks and upgrade risk management. It will also discuss the investment and loan policy for responding to each sector including carbonrelated businesses such as energy.

Metrics and Targets

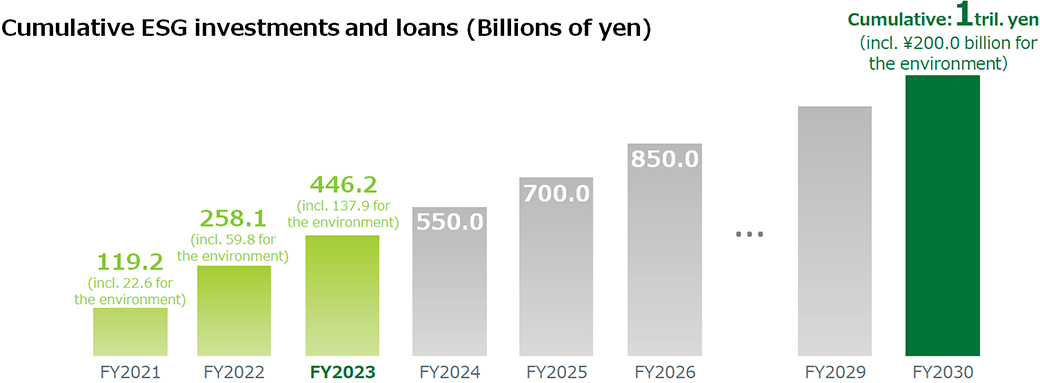

(1) ESG investments and loans

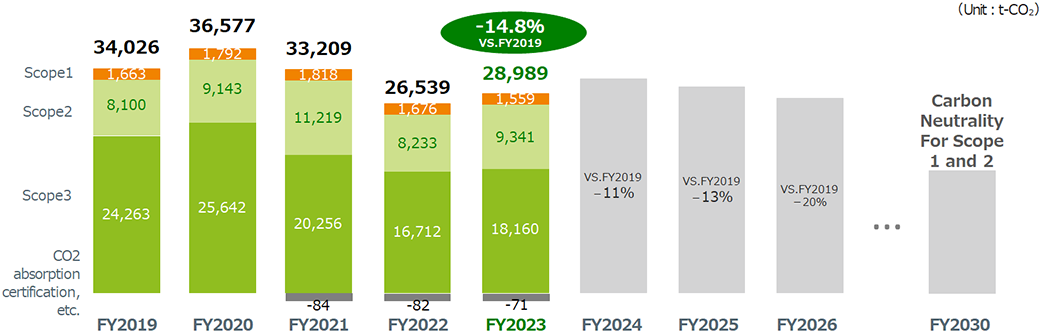

(2) CO2 emissions

- Carbon Neutrality Declaration

- Achieve carbon neutralityfor Scope1 and 2 by FY2030

- Scope of calculation: the Company and subsidiaries wholly owned by the Company

- CO2 Emission Reduction Targets

- By FY2026, vs. FY2019 levels-20%By FY2030, vs. FY2019 levels-30%

- Scope of calculation: The Company, Higo Bank and Kagoshima Bank

Targets: Scope1,Scope2, Category 1 (partially excluded), 3, 4, 5, and 12 of Scope 3

[Changes in CO2 emissions (target scope)]

[Changes in CO2 emissions (total emissions)]

| Measurement item | FY2019 | FY2020 | FY2021 | FY2022 | FY2023※ | |

| SCOPE1 | Gasoline, LPG, city gas, etc. | 1,663 | 1,792 | 1,818 | 1,676 | 1,559 |

| SCOPE2 | Market standards | 8,100 | 9,143 | 11,219 | 8,233 | 9,341 |

| (Reference: Location standards) | (10,785) | (10,966) | (10,120) | (9,185) | (8,614) | |

| Subtotal | 9,763 | 10,935 | 13,037 | 9,909 | 10,900 | |

| SCOPE3 | Total for figures below | 66,965 | 51,058 | 342,270 | 5,133,488 | 5,607,505 |

| Category 1: Purchased items and services | Stationery, copy paper, subcontracting services, advertising, etc. | 25,908 | 26,810 | 22,731 | 19,329 | 21,183 |

| Category 2: Capital goods | Property, plant, equipment and intangible assets acquired in the relevant fiscal year | 35,599 | 18,315 | 24,775 | 12,479 | 17,215 |

| Category 3: Fuel and energy-related activities not included in SCOPEs 1 and 2 | Gasoline, LPG, city gas, electricity | 1,988 | 2,105 | 2,023 | 1,840 | 1,794 |

| Category 4: Transport, delivery (upstream) | Postal fees | 409 | 375 | 372 | 346 | 378 |

| Category 5: Waste produced from business operations | Waste disposal fees | 675 | 964 | 68 | 72 | 58 |

| Category 6: Business trips | Business trips | 559 | 559 | 560 | 555 | 555 |

| Category 7: Commute by the employed | Commute | 1,307 | 1,329 | 1,330 | 1,316 | 1,316 |

| Category 12: Disposal of purchased goods | Disposal of bank books, PR items | 520 | 601 | 369 | 173 | 176 |

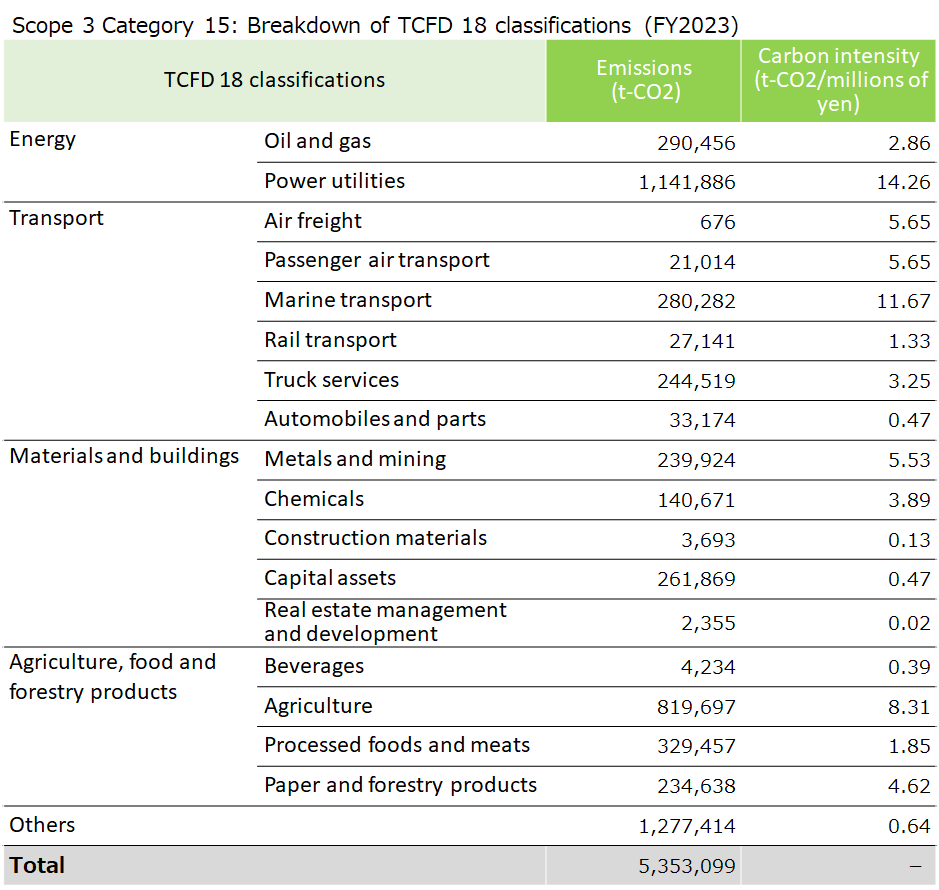

| Category 15: Investment | Listed stocks and corporate bonds | - | - | 290,042 | 205,872 | 211,731 |

| Business loans | - | - | - | 4,891,506 | 5,353,099 | |

| Total | 76,728 | 61,993 | 355,307 | 5,143,397 | 5,618,405 |

- Scope of calculation: The Company, Higo Bank and Kagoshima Bank

- The calculation of CO2 emissions is based on the GHG Protocol and uses the Ministry of the Environment’s Basic Guidelines on Accounting for Greenhouse Gas Emissions Throughout the Supply Chain, Emission Intensity Database Ver.3.3.

- The emission factors in Scope 2 are based on the emission factors by electric utility for the grid electricity of the project location (actual emission factors) as of the most recent date of the calculation.

- Emissions of Scope 3, Categories 8, 9, 10, 11, 13, and 14 were zero.

- Regarding Category 15

[Listed stocks and corporate bonds]

We used the Group’s investment balance as of March 31, 2024 and most recent, disclosed data on investees at the time of calculation (CO2 emissions and financial information on a consolidated basis). The calculation ratio of our Group's investments (based on market value) is 78.0%, and the data quality score by PCAF definition is equivalent to a score of 2. [Business loans]

From FY2022, we began using the measurement method proposed by PCAF in our calculations. The calculation ratio of our Group's loans is 98.7%, and the data quality score by PCAF definition is equivalent to a score of 4.

In the future, we will promote disclosure through bottom-up analysis by supporting CO2 emission measurement, etc.

(3) Others

- Number of certied basic decarbonization advisors

- FY20262,100

- Number of SDGs/decarbonization support projects

- Cumulative total for FY2024 to FY20262,250